Sebastian Heinermann (née Bleschke)

Managing Director

Contact:

+49 30 36418 086

info@energien-speichern.de

Foto:

studioline Photostudios GmbH

Renewable Gases are decisive in achieving our climate goals. Some sectors need green gases simply for technical reasons, others profit from economical advantages by using renewable gases. To tap their full potential, however, green gases need the right regulatory framework.

In the energy system of the future renewable or green gases can be used in a wide range of areas. Whether we look at biogas, green hydrogen or synthetical methane, the advantages of renewable gases speak for themselves.

Sectors like industry or transport for example need green gases simply for technical reasons. In these sectors renewable electricity cannot be used directly in many processes and machines. To achieve carbon-neutrality these sectors therefore need a green alternative: renewable gases.

In addition, green gases are economically beneficial for Europe’s countries. Looking at energy infrastructures renewable gases profit from the advantage of being able to use gas storage facilities and gas pipeline networks that already exist. The energy transition thus becomes more affordable for consumers.

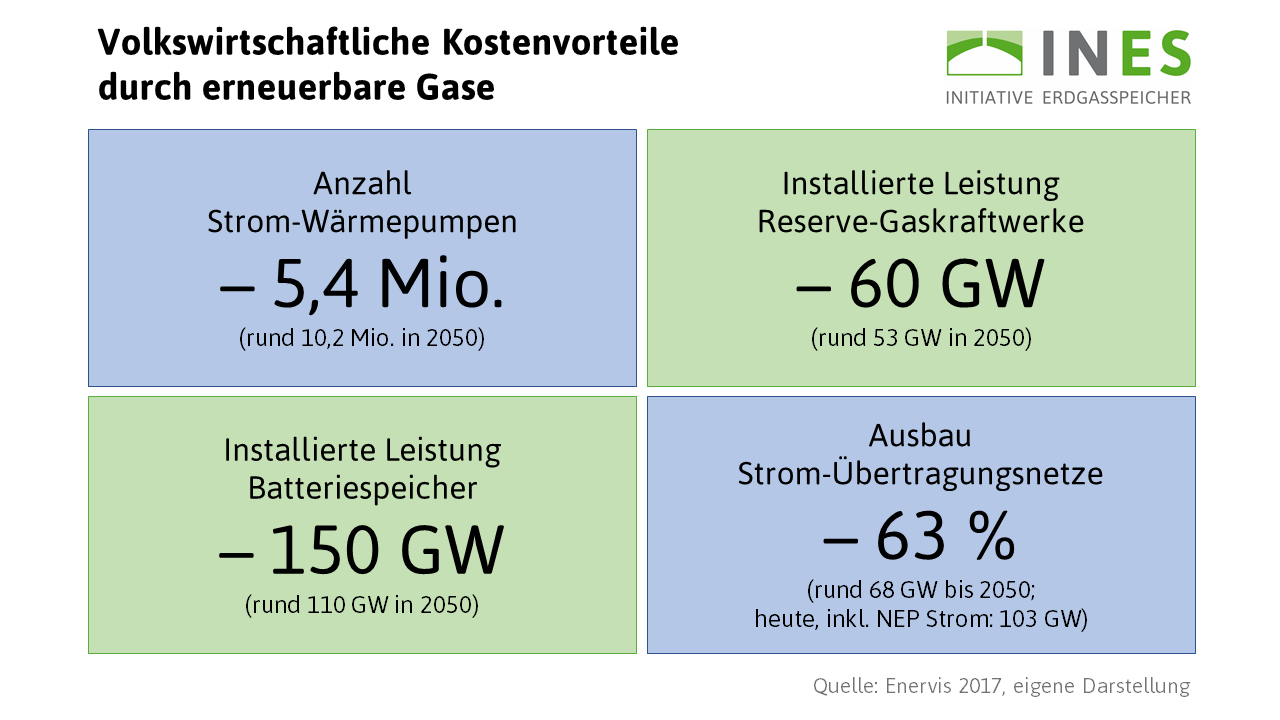

Regarding the heating sector in Germany for example, a study has shown that the need to invest in electricity grids can be reduced by two thirds if green gases are used as compared to an all-electric scenario. Moreover, the gas infrastructure holds a huge potential for storage and transport. Renewably produced electricity can be stored in gas infrastructures for long periods. Gas storage and gas networks thereby offer a solution for one of the biggest issues of the future energy system: the timely and spatial flexibility between energy demand and production.

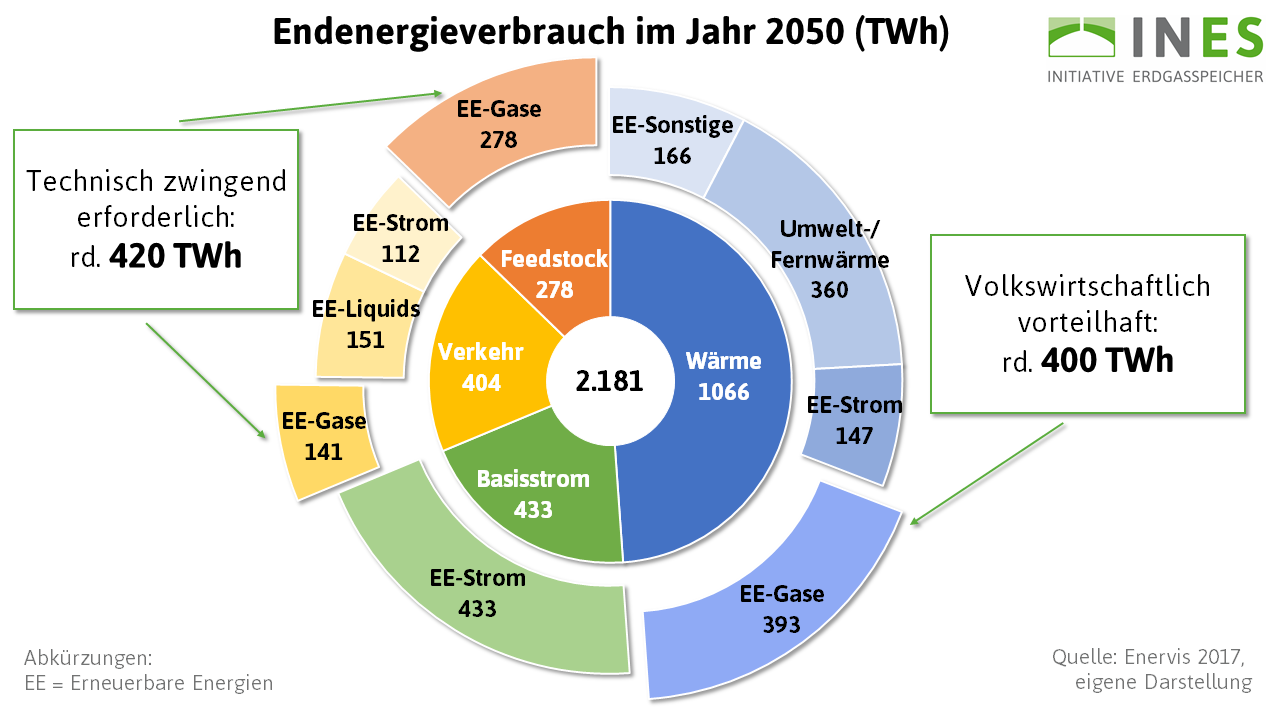

Many studies have shown the advantages of renewable gases on the way to a carbon-neutral society. A meta study of the VNG group on sector-coupling indicates that in Germany even in 2050 there will still be a relevant gas demand of more than 600 terawatt hours per year. To compare: In 2018 Germany’s gas demand hit 945 terawatt hours.

The Enervis study „Renewable Gases – a System Update for the Energy Transition” outlines the way to a carbon-neutral energy system in Germany until 2050. The paper shows that Germany should be using 930 terawatt hours of green gases to fulfill technical necessities but also decrease costs massively.

The more we move towards carbon-neutrality the more we will need renewable gases. Producing renewable gases with the Power-to-Gas technology therefore is a so-called deep decarbonization technology. As such we call technologies that allow us to reduce greenhouse gas emissions by more than 80 per cent.

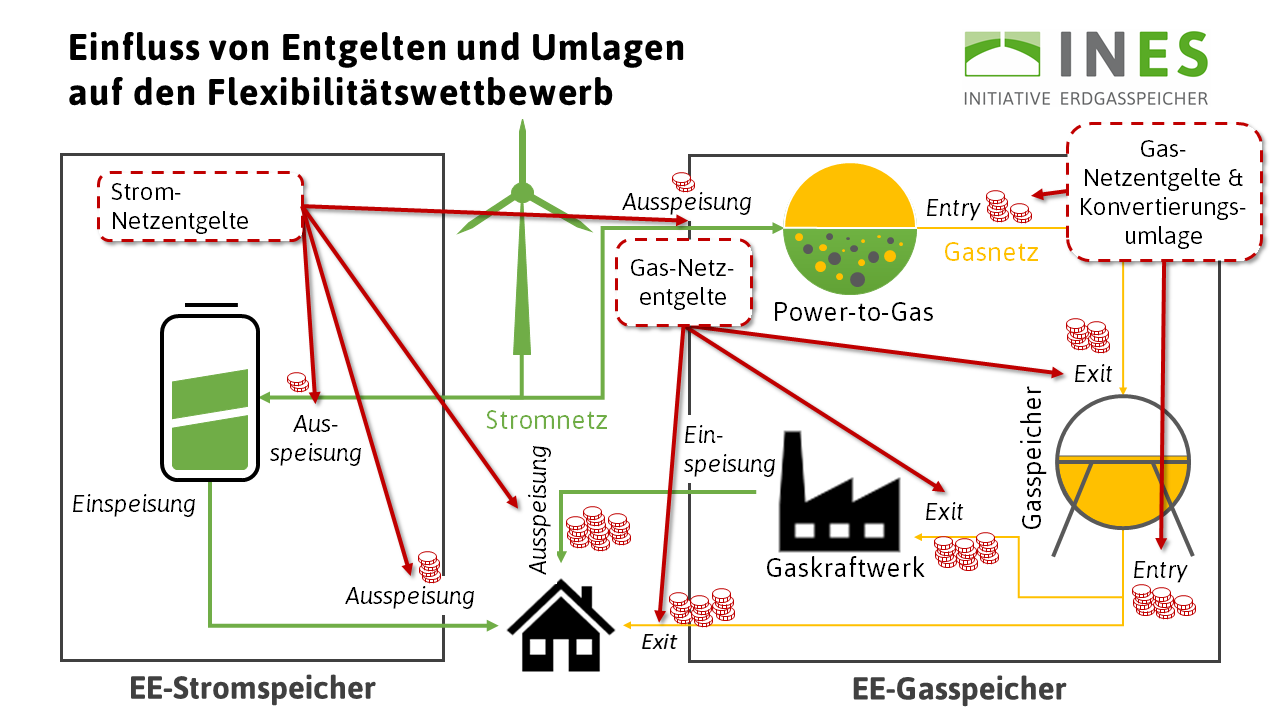

To develop a cost-efficient energy grid in the electricity as well as the gas sector, however, we need to think tariff structures of the energy grids more integrated. There must be an economical incentive for a Power-to-Gas facility to reduce the load of the electricity grid.

Therefore, most of the conducted studies assume that already in the years 2020 there needs to be a significant expansion of the Power-to-Gas infrastructure.

To design this development more cost-efficient, the production of green gases needs to become more affordable. Three fields of action can be identified to adapt the regulatory framework towards this goal:

Achieving the climate goals in certain sectors, in particular looking at the energy supply in the industrial field, can only be realized with renewable gases (or liquids). An affordable decarbonization path therefore requires a reduction in the costs associated with the production of renewable gases.

The market introduction of power-to-gas should therefore be promoted in such a way that renewable gases become competitive in a timely manner, that is to say in accordance with the requirements of decarbonization.

For example, to encourage start-up funding, network operators could identify system-relevant power-to-gas projects at connection points between the electricity and gas grids and tender this demand in a market-based process. Procurement of the capacity needed for existing needs will thus be as cost-efficient as possible. The costs for the system services could be refinanced via network charges. This procedure has the advantage that the competencies of the market players for the construction and operation of power-to-gas plants are developed under competitive conditions. In addition, market-led power-to-gas plants are not limited exclusively to the use of renewable gases as a system service.

Consumers will – in the future as well as today – need energy, even if there is no wind or sunshine. However, the so-called residual loads, i.e. the energy demand, which arises independently of the volatile energy carriers such as wind and sun, must nevertheless be covered from renewable sources. Green gases are the optimal solution for this.

As seasonal flexibility providers for renewable energies, gas storage system operators will also play an important role in the energy system of the future as they can store renewable gases over short, medium and long-term periods.

However, the legal framework of the competition for cross-sectoral flexibility is currently designed in a discriminatory manner – especially in relation to gas storage and electricity storage. Charges, levies and taxes should therefore be introduced without discrimination across sectors. For this purpose, levies, especially if they are levied to avoid greenhouse gas emissions, should only be incurred at the level of final energy consumption. The conversion or storage of energy should not be defined as final energy consumption. In addition, opportunities to be relieved from charges, levies and taxes under the regulatory framework should benefit all flexibility providers. It is only under these conditions, that state-designed charges will not distort cross-sectoral competition in the flexibility market.

A decarbonization path based solely on electricity requires – as politicians have already realized – considerable investments in the electricity infrastructure, i.e. electricity transmission and distribution grids. These investments can be significantly reduced by using green gases instead.

In order to develop an economically optimal energy network from electricity and gas infrastructures, however, the system of network charges of the electricity and gas sectors also have to be integrated. Ultimately, it must be worthwhile for a power-to-gas plant to relieve the power grid from loads. Network charges should therefore be established in both the electricity and gas sector in such a way that market decisions ensure a cost-effective network use across sectors.

Regulatory requirements for the network development are also necessary. The grid development for the electricity and gas sector, which is currently being carried out separately, should be planned in an integrated manner in the future. To this end, the scenario development reports and network development plans should be developed across sectors. The joint network development must then take place, taking into account a cross-sectoral, cost-efficient use of the network. To achieve this, the costs of grid expansion must be compared across sectors and weighed against each other.

Sebastian Heinermann (née Bleschke)

Managing Director

Contact:

+49 30 36418 086

info@energien-speichern.de

Foto:

studioline Photostudios GmbH